Harvest Sideways Volatility?

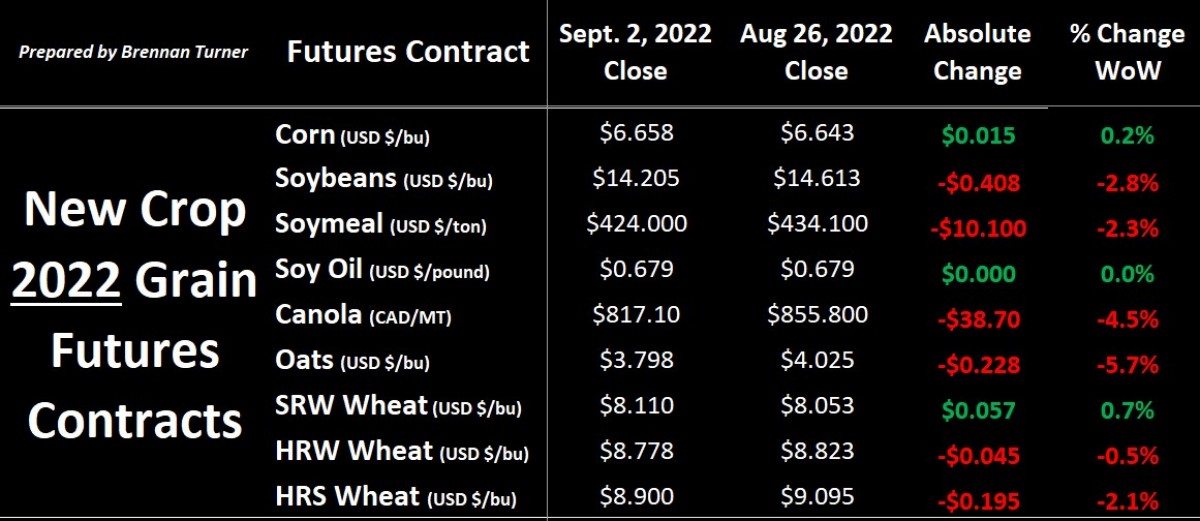

Grain markets were mixed to start the month of September, with gains on Monday and Friday last week offsetting the selling through the middle of the week. The futures markets of Western Canadian crops like spring wheat, oats, and canola continued to see lower values after last week’s production estimates from Statistics Canada suggested a healthy pipeline of supply for the 2022/23 crop year (more on this in a bit). Ultimately, we’re getting into the throes of Harvest 2022 so, despite the obvious field delays, I expect more sideways trading in the coming weeks (unless a government report provides a surprise…).

Thanks to the wet, late start, and recent rains and humidity, the Manitoba harvest is only at 3% complete, well below the average by this time of year of 39%! Comparably, in Saskatchewan, 23% of all crops are now in the bin, only slightly behind the five-year average of 26%. Still, eastern Saskatchewan continues to have the same rains that Manitoba has been getting, meaning crop dry-down hasn’t happened and harvest activity has been similarly delayed. Finally, in Alberta, 17% of the major crops have been combined, slightly above the seasonal average of 13%, but behind last year’s early drought-impacted harvest of 26% by the start of September. It should be noted that Environment Canada has predicted average to above-average temperatures for Western Canada from September to November, suggesting that Mother Nature could play nice for a delayed harvest. Across the border, as of last week, the U.S. spring wheat harvest is now 50% complete, 21 points its normal pace, but Minneapolis HRS futures did drop on the week.

The U.S. corn crop’s good-to-excellent ratings dropped another point last week to now sit at 54% G/E, which is partially why hedge funds increased their net long in corn last week to their largest position since the end of June. There are also many consensuses that the USDA will reduce their average corn yield estimate in their next WASDE report, published on Monday, September 12, 2022. While the trendline yield estimate back in their February Outlook was 181 bu/ac, the USDA pegged things at 175.4 in the August WASDE, which is much higher than private estimates from ProFarmer’s crop tour of 168.8 bu/ac and DTN’s “digital crop tour” of 167.2 bu/ac. Even if the average yield came in around 170 – 172 bu/ac, without demand changing, 2022/23 U.S. corn carryout would likely fall below one billion bushels, a very tight supply situation (I’m sharing this as, with higher corn prices, more, cheaper wheat could go into feed rations instead, thereby supporting wheat prices a bit).

Looking abroad, Brazil is likely to plant a very large corn crop this year, but those supplies won’t come to market for at least another 9–10 months. Meanwhile, the French corn crop is experiencing its lowest rating in over a decade as recent rains won’t help improve yield potential after a hot summer. Another area I’m watching is northern China as drought conditions have threatened current and future crop production potential. The region is responsible for about 35% of China’s total cotton production, 45% of its corn, and 60% of its wheat harvest. Still, groundwater levels have gotten so low that it’s putting aquifers at risk of collapsing. This has also led to hydropower plants in the region operating at as little as 50% of their normal capacity (which has led to a manufacturing slowdown in the area). Needless to say, the last few months of hot weather in the northern hemisphere could create challenging soil moisture situations for not just fall seeding, but also the spring.

In the Black Sea, Ukraine has now shipped out about 2 MMT of grain on 86 ships to 19 different countries since the “grain corridor” deal for safe passage through the Black Sea was announced back on July 22, 2022. This past week, the Ukrainian Ministry of Agriculture suggested that they could export 50 MMT in 2022/23 (off a 60 – 65 MMT harvest), but asterisked their forecast in saying that that volume could take up to two years to ship out if ports are not operating properly. Suffice it to say, if any military operations escalate again, an export activity could be halted overnight, but the market is currently trading with little-to-no premium for this type of risk.

One other risk that commodity markets are starting to price in is an economic recession and rising interest rates. With inflation in most first-world countries running at multi-decade highs, and thanks to governments pumping trillions of dollars of COVID stimulus dollars into the economy, central banks are now rising interest rates every few months! Historically speaking, there’s usually an inverse relationship between interest rates and commodity prices, meaning as interest rates rise, commodity prices tend to drop, and vice versa. With interest rates increasing today to offset high inflation, there’s an increased incentive to bring supplies to market today, rather than later and thereby, carrying less inventory (AKA less “cost of carry”). Further, interest rate hikes tend to see a country’s currency appreciate, meaning their goods become more expensive for international buyers, potentially leading to lower demand. Some

However, with almost every major central bank raising interest rates, and still-tight supply chains, I think that demand will remain strong, but there are some major headwinds that economies are facing. In Europe, energy prices have skyrocketed thanks to their dependence on Russian supplies – i.e. French power prices are trading 30x their 5-year average! Thus, manufacturing companies from beer to fertilizer makers are idling their facilities as the cost to produce goods is now much greater than what they can sell their goods for. This means people will be laid off, and while they may just be temporary, this has a trickle-down effect in many other areas of the economy. Obviously, with smaller fertilizer supplies – including the likes of China, Russia, and others limiting or outright restrictions of exports – this could have negative impacts on both the global Harvest 2023 potential, as well as the basic supply of foodstuffs!

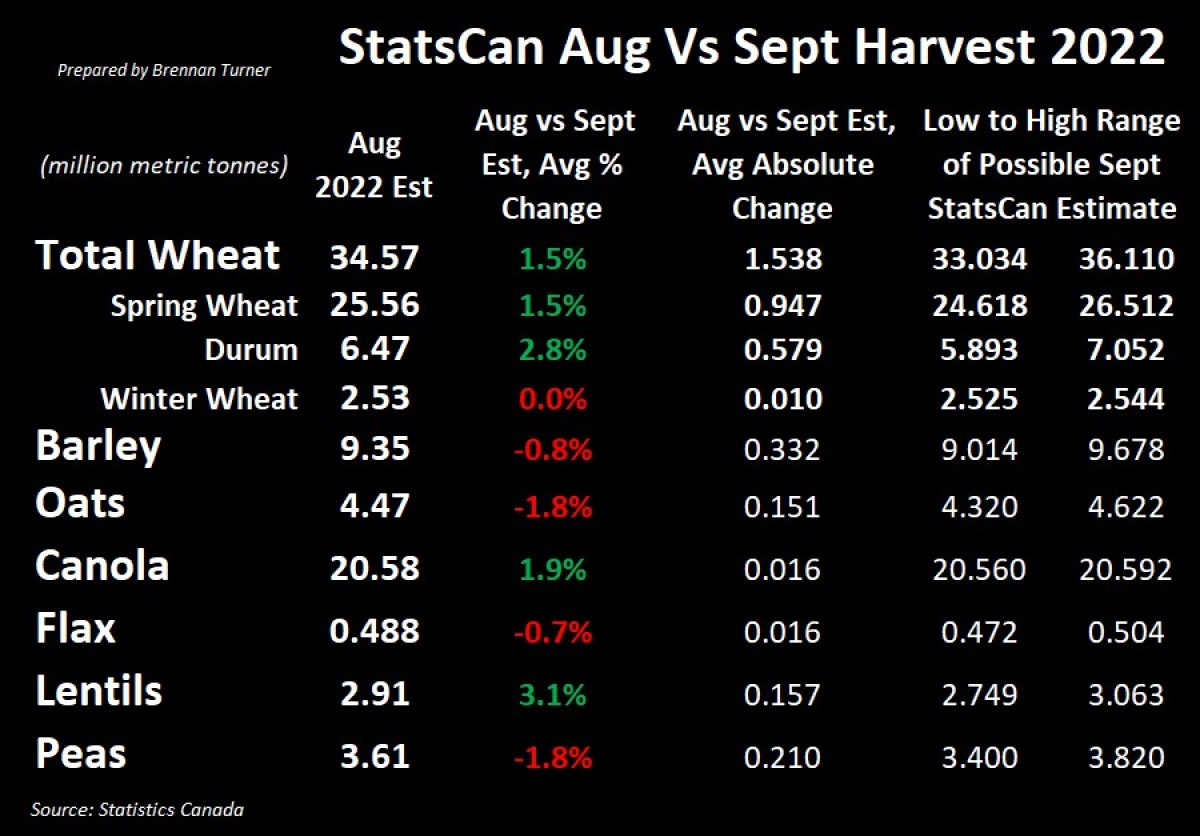

Coming back home and ahead of next Wednesday’s production estimates update from Statistics Canada on September 14, 2022, I wanted to show how much these harvest estimates change from report to report. For context, StatsCan puts out three crop production estimates every year: one at the end of August, one in mid-September, and one in early December. While I can only assume that the data science team at StatsCan is getting better with every estimate they make, if looking at the average of the last five years, including last year’s drought, the Canadian wheat crop tends to get bigger as time goes on.

More specifically, from the August to September estimates, StatsCan tends to increase the size of the spring wheat crop by about 1.5%, with an average change of nearly 950,000 MT in the few weeks between their publications. For durum, StatsCan also underestimates production by nearly 3%, with an average change in August to September estimates of 580,000 MT. I should note here that StatsCan lowered the spring wheat and durum crop size in their 2020 and 2021 August vs September estimates, but increased them in the previous three years (2017 – 2019). On the flip side, the winter wheat crop is basically known by this point of the year (with almost everything in the bin), so no changes are really seen.

Therein, volatility remains a looming factor going into the thick of Harvest 2022. With regional droughts, the war in Ukraine, and the expanded money supply, greater trading ranges could be expected. This is because, with greater risk in the markets, traders reduce their exposure to said market happenings. Still, with less money/participants in said market, this will amplify trading volatility. Unfortunately, none of us can control these happenings, so instead, I encourage you instead focus on staying on top of your harvest to-dos, taking good samples from every load as they go into the bin, and checking with your buyers for delivery times.

To growth,

Brennan Turner

Founder | Combyne Ag