A Dry Start to Plant 2024’s Acreage Plans?

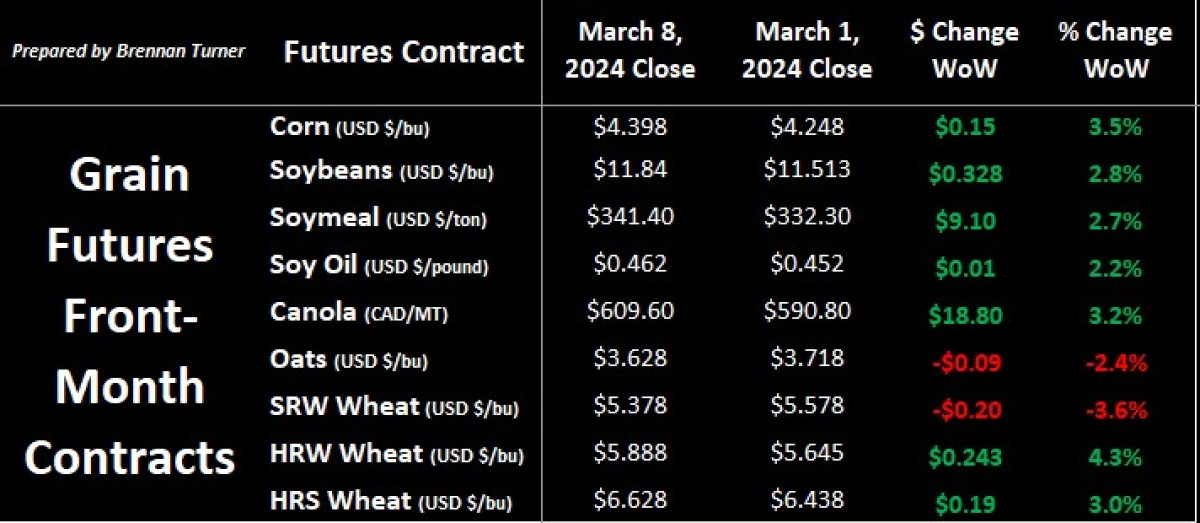

Grain markets continued to trend lower at the beginning of March but have been impacted by this month’s WASDE report. The complex now appears to focus on southern hemisphere production and is considering the potential impacts for the 2024 growing season. With a slightly neutral report from the USDA and managed money holding near-record short positions for corn, soybeans, and wheat, we saw a nice rebound to finish the week.

Despite the Chinese cancelling quite a few boats of Chicago-traded SRW wheat (about 4M bushels), the hard varieties maintained some strength. We will need to see more momentum this week as we’ve seen this story many times over the last year, with lots of profit-taking on short-term rallies. Statistics Canada’s acreage estimates, which were just published on March 11, won’t have much impact as there aren’t many changes compared to last year, except for oats acreage jumping 22 per cent year-over-year to 3.1M.

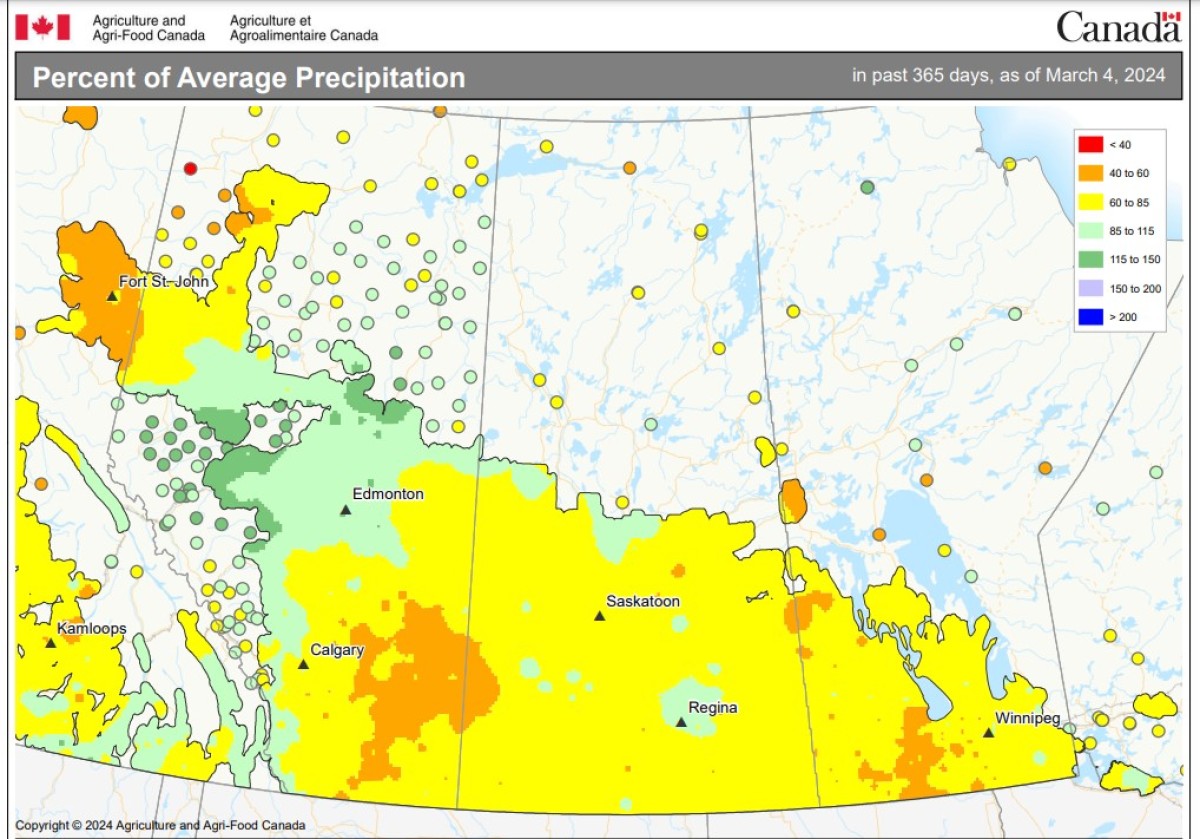

Speaking about what Grow 2024 could be impacted by, the U.S. Climate Prediction Center is now expecting a transition to a strong La Nina by fall, but neutral conditions for most of spring and summer. This usually means benign growing conditions, right? Well, since 1950, in the five times that we’ve seen a switch from a strong El Nino to a strong La Nina, it’s typically led to above-average spring temperatures in the U.S., especially the Northern Plains. The good news is that June has the potential to be pretty wet for the northern areas, and even though we got a nice dump of snow last week, everything south of the Trans-Canada highway is still looking for moisture. Through to March 4, below is a map of the last 365 days of moisture in the Prairies, relative to the average.

WASDE & Other International Wheat News

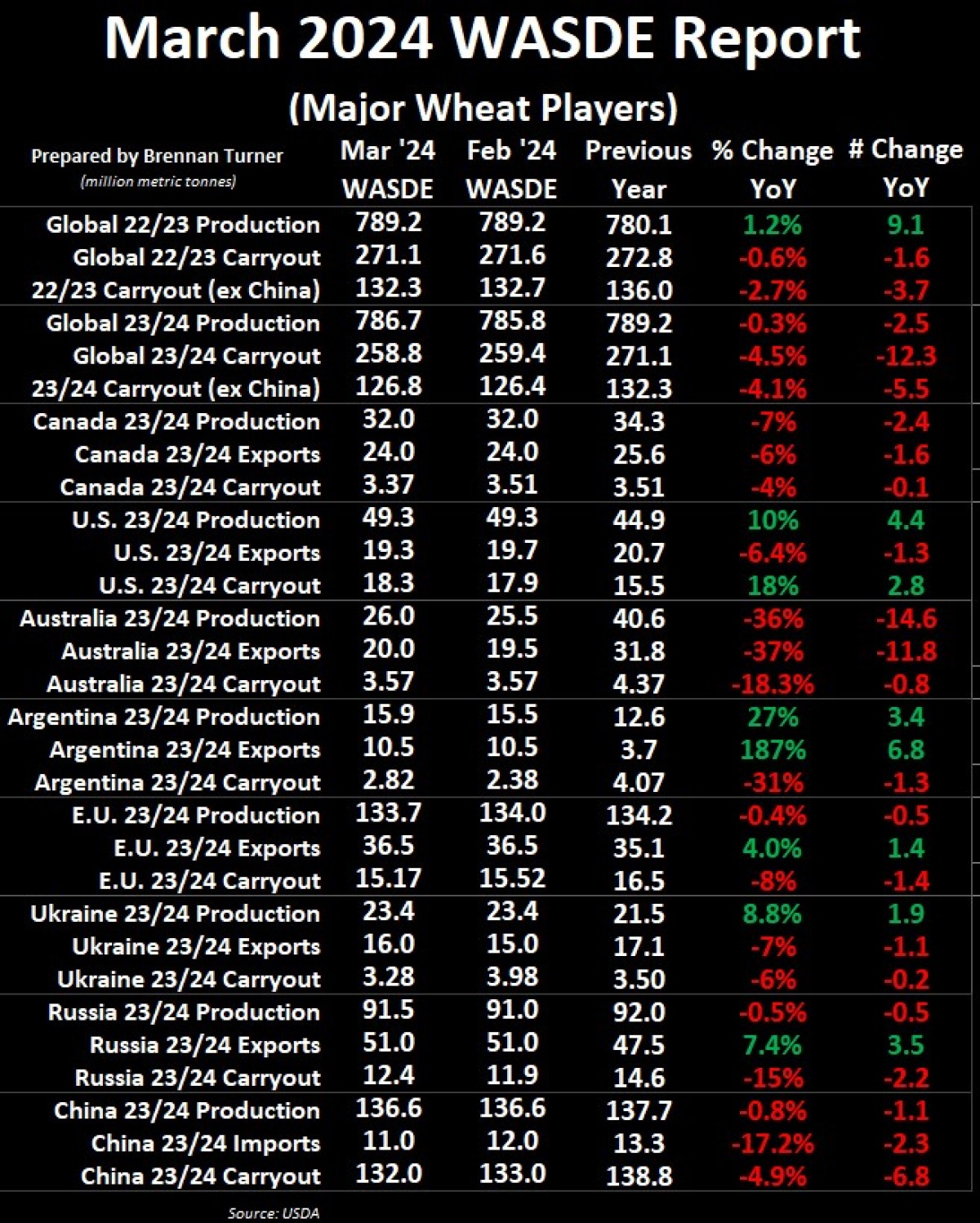

• Nothing substantially changed on the 2022/23 balance sheet, but the USDA did raise its forecast for 2023/24 production by nearly one million tonnes but lowered global ending stocks by over 600,000 MT on higher trade.

• U.S. wheat ending stocks were raised by 15M bushels, wholly attributed to winter wheat, whose exports were lowered by the same amount.

• Australia’s production was raised by 500,000 MT to 26 MMT, and with the harvest over, they exported over 2.7 MMT of wheat in January, with China and Indonesia being the two largest destinations.

• Ukraine wheat exports were raised by 1 MMT to 16 MMT, but Ukrainian President Volodymyr Zelenskyy warned that the Black Sea shipping corridor could close without U.S. military help, something we’ll keep an eye on as the November 2024 U.S. Presidential election approaches.

• Russia’s production was raised by another 500,000 MT to 91.5 MMT. They shipped 3.8 MMT in February (a record for the month). They also reiterated last week that they don’t care about renewing the Black Sea Grain Deal.

• Western Europe remains pretty wet after a soggy February, and France’s soft winter wheat good-to-excellent rating of less than 70 per cent is the worst in four years.

Strong Wheat Demand Doesn’t Mean More Acres

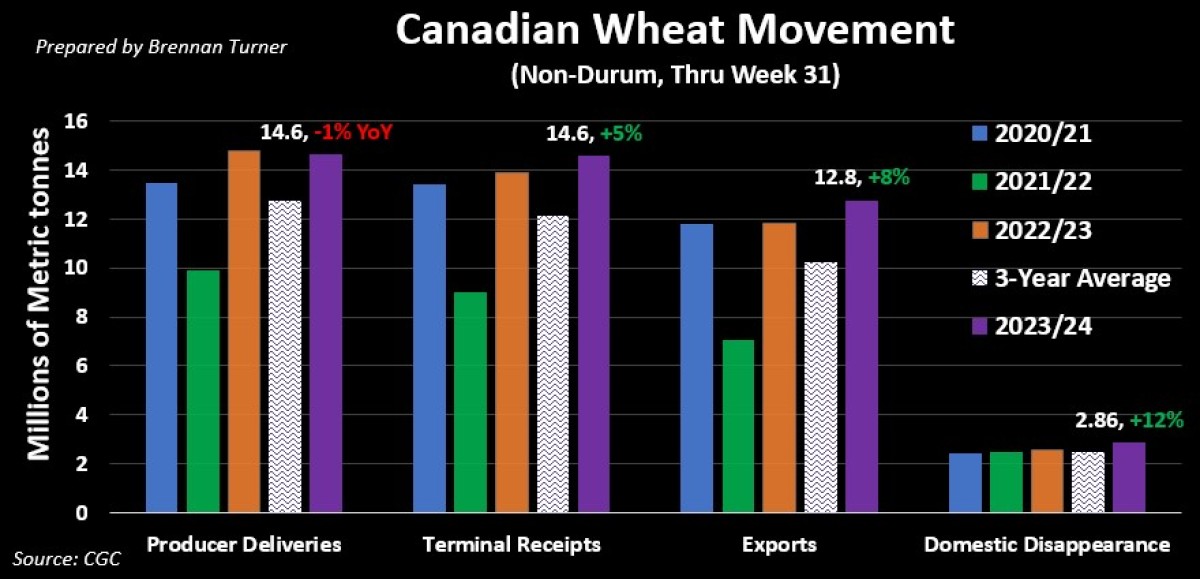

• Through week 31 (start of March), Canadian non-durum wheat exports continue to track well, up 8 per cent year-over-year with a weekly average of nearly 412,000 MT, meaning about 356,000 MT of weekly sailings are needed to meet AAFC’s full-year target of 20.25 MMT

• Worth noting that in the last 13 weeks (or quarter) of the crop year, Canadian wheat exports are usually about 10 per cent lower than the weekly average of the previous 39 weeks.

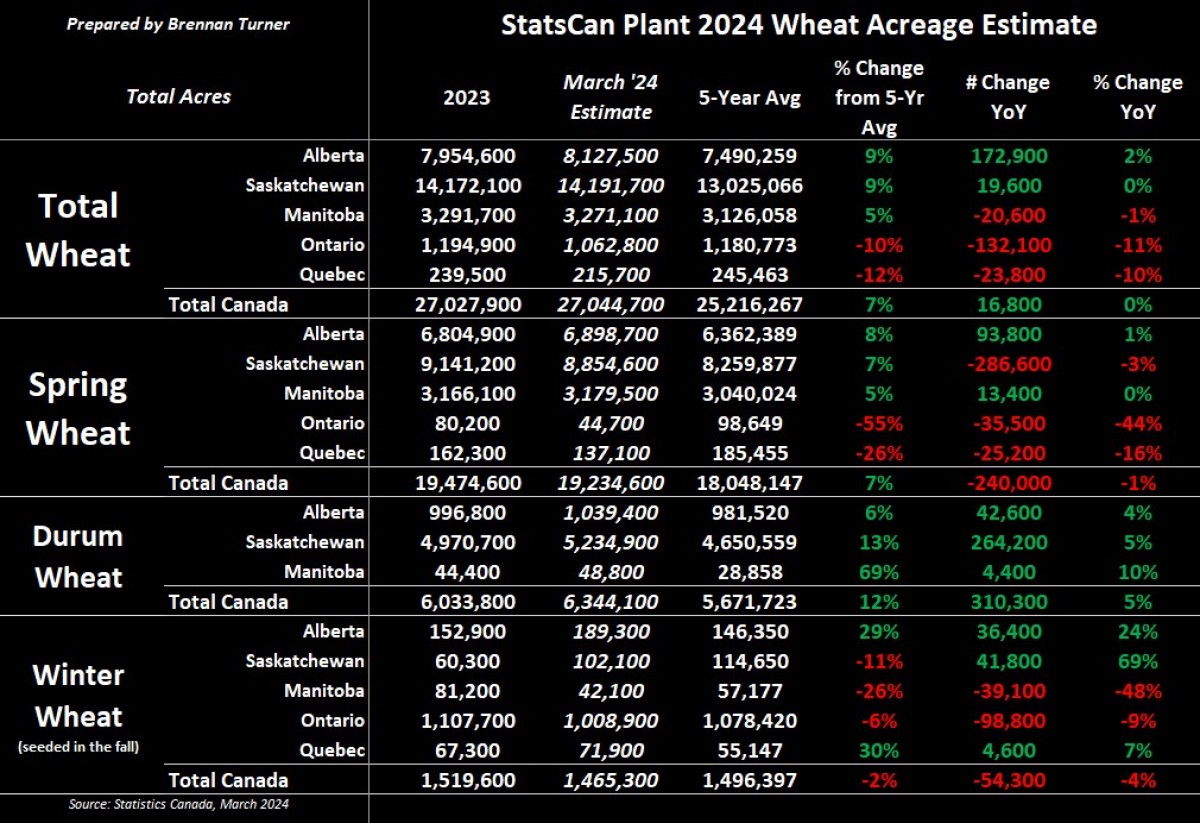

• StatsCan said that farmers will plant 19.2M acres of spring wheat and 1.5M acres of winter wheat, down 1.2 per cent and 3.6 per cent, respectively, year-over-year.

• Most of the decline for spring wheat is in Saskatchewan, while Ontario says almost 100,000 fewer winter wheat acres were seeded last fall because of how wet it was.

Durum Acreage Up, Exports Down

• Canadian durum acreage is set to expand by 5 per cent to 6.3M acres, with the bulk of the expansion coming in Saskatchewan (and likely taking over some of the spring wheat areas there).

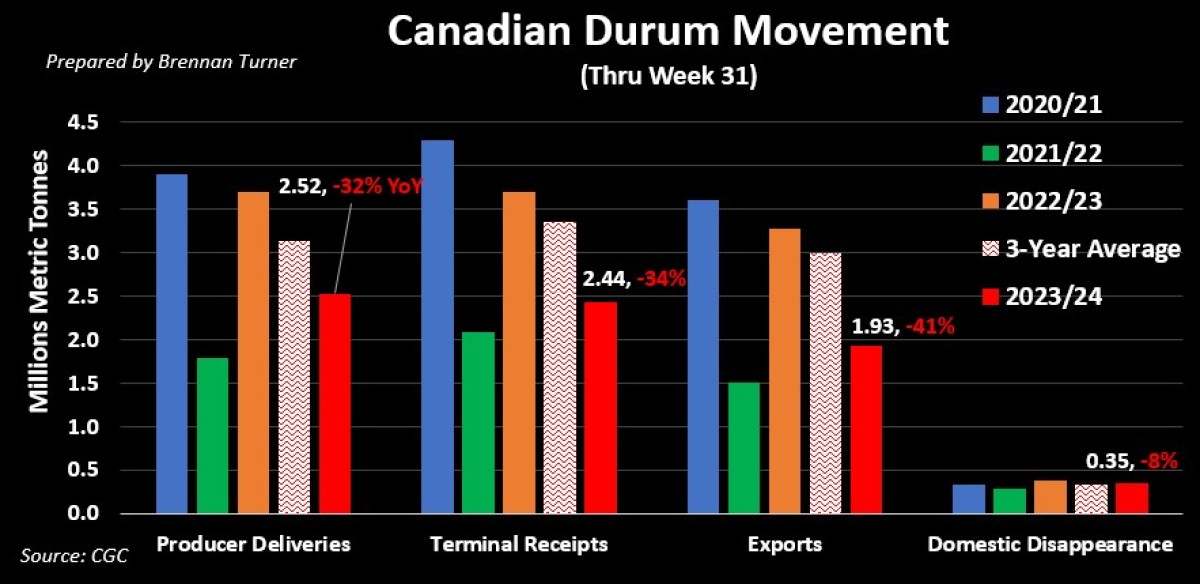

• In the WASDE, U.S. durum imports were raised by 4M bushels to 44M bushels. Conversely, through January, Canadian durum exports to the U.S. are tracking 36 per cent lower year-over-year.

• Canadian durum exports have been slowing down, from over 71,500 MT per week a month ago to now just over 62,300 MT, which means that to reach AAFC’s crop year target of 3.2 MMT, week shipments will need to average 60,400 MT every week (compared to just about 51,000 MT a month ago).

• While Canadian wheat exports tend to slow down in the last quarter of the crop year, durum exports actually rallied by about one third over the last three weeks.

• Turkey issued another tender last week to sell 150,000 MT of durum, indicating their export program has no signs of slowing down.

• During France’s annual agriculture conference, the government announced a plan to improve self-sufficiency in the pasta crop. They have committed nearly $63.5M Canadian to be invested over the next five years with a goal to increase domestic demand needs from the current 35 per cent to 45 per cent, effectively reducing imports.

• Latvia became the first EU country to ban all Russian agricultural imports; up until now, Russian durum exports to the EU so far this year are tracking about nine times higher than last year, with over 400,000 MT being imported.

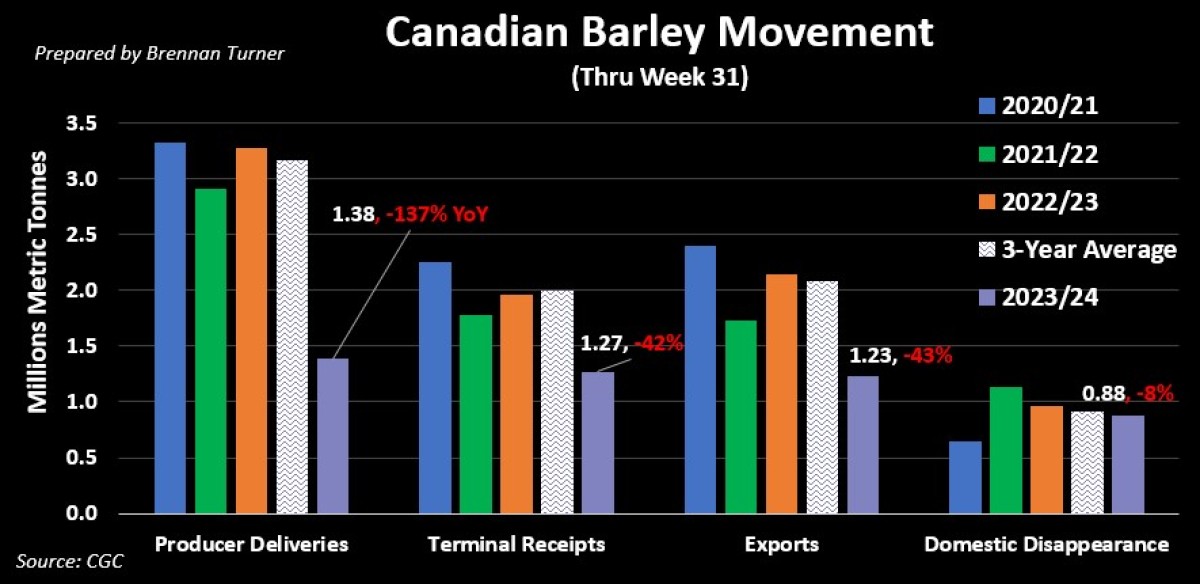

Canada Barley Acres Retreat with Prices

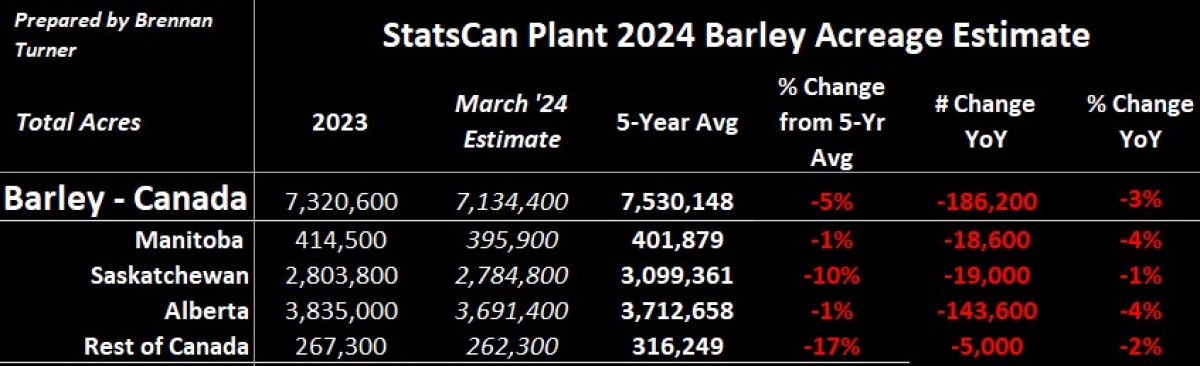

• Canadian barley acres are expected to fall by 2.5 per cent year-over-year to 7.1M acres, most likely at the expense of the rise in oats area.

• Generally-speaking, the price of all feedstuffs, including corn and soymeal, hasn’t been this low since 2019, which means we’re likely going to see more buyers moving away from buying only as needed.

• Internationally, this includes China, who is intent on buying on the lows, including more than 20 cargoes of feed grain in the past two weeks alone (or 1.2 MMT).

• With weak corn prices in Europe, the incentive for more barley being planted this spring is real, mainly of malting varieties, but wet conditions may mean less acres than initially anticipated this winter.

To growth,

Brennan Turner

Independent Grain Markets Analyst