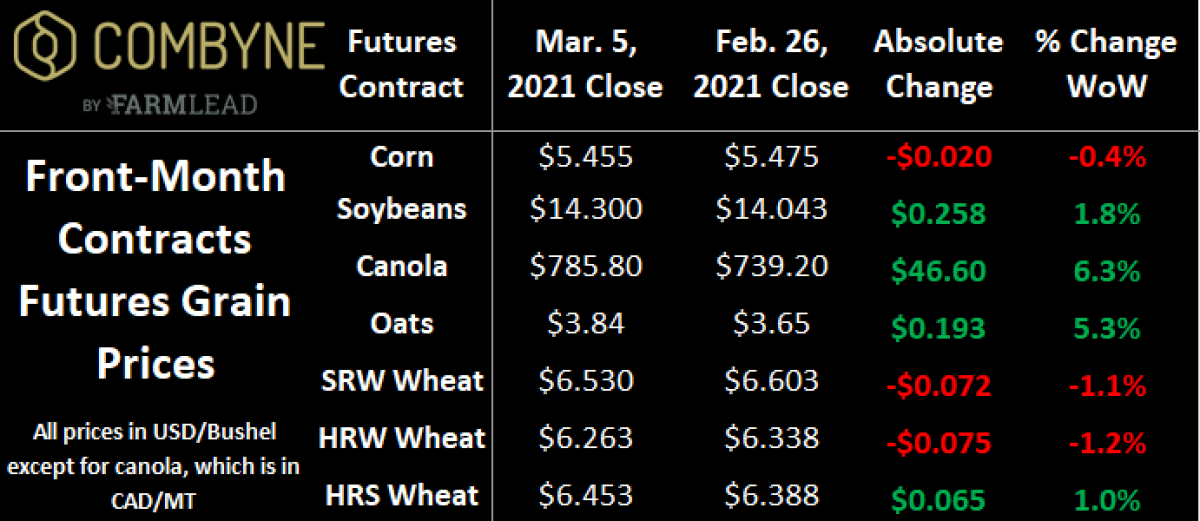

Fireworks or Just Sparklers?

On the flipside, meteorologists in Argentina continue to be concerned about the dry weather they’re seeing. On Tuesday, March 9th, the USDA will publish their updated WASDE numbers, but as we all know, the numbers in it reflect the conditions from a couple of weeks ago, and not the present, hence continued uncertainty about production in South America, and thus continued volatility in grain markets. Going into the report, expectations are that global soybean ending stocks will fall, while wheat carryout will be increased yet again.

Beyond the current crop year, a lot of the attention for bigger global stocks is being attributed to the EU and Ukraine. For the latter, the Ministry of Agriculture there said last week that they expect record wheat exports in 2021/22 of 22 MMT, which would be about a 25% increase over the 2020/21 projections. The increase in exports is a natural by-product of what the Ukrainian govt thinks could be a record total grain crop in 2021/22, including 29 – 30 MMT of wheat (they harvest 25.1 MMT in 2020/21).

Over in France, FranceAgriMer says that the winter wheat crop there is looking pretty good, with 88% of the crop rated good-to-excellent, which is materially better than the 64% rating seen at this time a year ago. Further east in Russia, a milder winter has dropped the percentage of fall-seeded crops in bad condition from 22% in early December down to about 8%. While that’s still 4 points higher than what they saw a year ago, keep in mind that there were quite a few more acres seeded this past fall.

Ultimately, wheat prices continue to be supported by uncertainty related to new crop production and weaker export competition, now that Russia is basically out of the market until they start taking their 2021 crop off. More explicitly, we’re at the time of year where there’s a lot of uncertainty in the market as it relates to the coming year’s production volumes. While we can make mathematical guesstimates, Mother Nature continues to hold the final say and thus, uncertainty tends to bring higher values.

Therein, there are more than a few pockets in North America that are entering Plant 2021 with some level of drought condition. Combine this with the fact that the U.S. Climate Prediction Center is suggesting that there is a 60% chance that the current La Nina conditions could transition to more a neutral environment, meaning that a warmer/drier spring could materialize. However, this also means that there’s a 40% chance the current La Nina trend will continue, meaning the spring could be cool and wet. Basically, fireworks in wheat markets are a possibility, but so are sparklers.

Ultimately, from my vantage point, if there is any weather scare in North America, new crop grain prices could be amplified by not just the supply concerns, but also the continued increased demand related to COVID over-buying. Thus, I’m probably not going to be more than 35% - 40% sold on my wheat going into the planting campaign as I feel this is a healthy middle ground. Why? If there are no weather issues, then I’ve locked in a healthy percentage of my expected production at a profit and for delivery at harvest to ensure cashflow, all with the likely expectation that prices fall around that time of year. On the flip side, these are profitable sales at great prices (relative to last year and the seasonal average), and should the market rally significantly during the growing season, I can still make additional sales! We’ve been getting some great feedback on our new Target Offers tool, in that if you’re not watching the markets every hour, consider using it to put in a customized freight and target with up to 10 of your buyers!

To growth,

Brennan Turner

CEO | Combyne Ag

Combyne.ag