Russia Invaded Ukraine; What Happens Now?

Grain markets, like almost every other market this past week, saw plenty of volatility as Russia started its unprovoked invasion of Ukraine. Ultimately, like every one else, I suggested in this column a few times (specifically 2 weeks ago and a month ago) that the likelihood of a Russian invasion was about 5% - 10%, but it’s clear we all underestimated Putin’s willingness to go to war. In the below, longer-than-usual column, I will try to simplify a very complex, intertwined situation, but I caution that things are evolving on an hour-by-hour basis, and in some areas, minute-by-minute. Practically speaking, where grain markets go next could change very quickly.

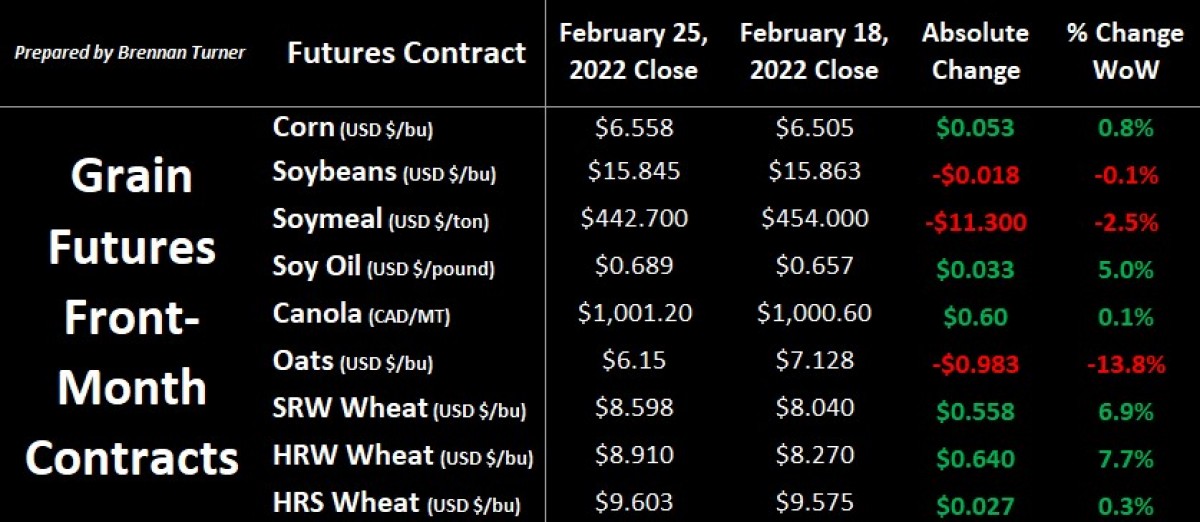

This volatile environment was on full display last week as the wheat complex sped higher Wednesday night on the invasion news, with front-month contracts then closing limit up on Thursday. This included Chicago wheat futures briefly topping their 2012 highs while Paris wheat futures hit their own new record high. For Friday’s session, trading limits in Chicago and Kansas City wheat futures were expanded to 75¢ USD/bushel. Since traders recognized the incredibly volatile situation, no one wanted to hold their positions going into the weekend. Thus, we saw a massive sell-off across the grains complex but especially in wheat markets, which went limit down, just one day after going limit up (including Minneapolis HRS wheat, whose limit is 60¢). While the below table shows grains’ weekly performance, these were Friday’s one-day changes for the front-month May 2022 contract:

- CHI SRW Wheat: -75¢ USD/bu

- KC HRW Wheat: -75¢ USD/bu

- MGE HRS Wheat: -60 USD/bu

- Corn: -34.5¢ USD/bu

- Soybeans: -69.5¢ USD/bu

- Canola: -$50.80 CAD/MT

- Oats: -38.75 ¢ USD/bu

- Soymeal: -$12.9 USD/ton

- Soy Oil: -$0.03 USD/lbs

I’ve been reading a lot of material these last few weeks as to why Russia would want to invade Ukraine. Apart from all the agricultural, mining, and deep water port assets in Ukraine, Russia is responsible for supplying Europe with about 40% of its natural gas needs (including Germany, which relies on Russia for about 2/3s of its natural gas). The delivery of this natural gas is done via two aging pipelines, one through Belarus and the other through Ukraine, the latter of which Russia pays Ukraine about $2 Billion USD a year in transit fees. Russia is a petrol-state with 40% of its national spending attributed to oil and natural gas revenues, so securing the pipelines is in their economic interest. Worth noting here is that Belarus is politically aligned with and supported by Russia, and this is why Russian military forces have pushed into Ukraine via Belarus. It’s also probably also why Belarussian military forces are now documented as joining the invasion of Ukraine.

Ultimately, multiple markets are in high-risk scenarios, including food, fertilizer, energy, and especially financial markets, given that the 11th-largest economy in the world is essentially being isolated from SWIFT, the international payment processing system and one of the key pipes in the global financial system’s plumbing. Cutting many Russian players off from SWIFT will impact the flow of payments for every industry that Russia is involved in, ranging from the jet engine and automotive manufacturing to exports of wood, palladium, nickel, grain, and fertilizers.

For the record though, some Russian banks have been excluded from the fullest extent of these sanctions, including Gazprombank, which is responsible for serving large oil and gas payments. If you’re wondering why some Russian institutions are exempted, Russia touches a significant amount of the global energy market and so, political leaders are aware of the negative impact on Western economies, especially since energy, notably retail gasoline prices, are already hitting record highs today.

Put in the simplest terms, Canada, the U.S., and others will continue to import Russian energy (despite North America ironically having the means to be independent of it), but Europe is extremely energy-dependent on Russia. If these flows were cut off to Europe, there would be no short-term solution to replacing this energy. In this scenario, many strategists estimate that military invention by NATO members is quite likely (basically suggesting the situation could get much worse/violent).

Compounding the financial situation is restrictions on the Russian central bank’s international reserves of $640 Billion, nearly half of which are held abroad in places like Europe, the U.K., and America. Globally, people are furiously looking to unload their depreciating Roubles (not to mention, just trying to get their money out of Russian banks, which leads to bank runs), and as they’re sold, the supply of the Russian currency increases. However, demand falls with very fewer interested buyers of the Rouble, meaning the value of currency weakens further. As an analogy to grain markets, think of it like if a bumper harvest happened, but no one wanted to buy the grain, market prices for the grain would plummet.

This is where the Russian central bank would step in to stabilize the currency and buy up Roubles using their own international reserves as they did in 2014 during the annexation of Crimea. But if the Russian central bank runs out of reserves, or you don’t have access to them, the Russian Rouble effectively goes into a tailspin, which is what we’re seeing happen before our eyes, similar to what happened in Russia’s August 1998 financial crisis. Almost always, in these situations and, as was the case in 1998, economic depression and major inflation results, basically meaning that value of Russian exports falls, as does their own international purchasing power. One scenario that needs to be mentioned, and could complicate things even further, is if Russia turned to China for financial and economic help, and it is a real possibility if Putin has nowhere else to turn.

This condensed explanation of the financial situation should help give some better context to the impact on grain and fertilizer markets, which is quite material as there are 3 core areas of disruption. First, in the fertilizer markets, we already know that China and Russia are banning phosphate/urea and nitrogen exports, respectively, until June 2022. With so much uncertainty in available/exportable/purchasable fertilizer, these export bans could be further extended. Further, with Belarus now involved, it’s likely that potash exports from both them (the #3 producer) and Russia (the #2 producer) will be either sanctioned or go offline completely.

Yes, Canada is the number one potash producer in the world, extracting basically the same amount as Russia and Belarus combined. However, with fertilizer prices already high, and the northern hemisphere about to plant its 2022 crop and/or additional fertilizer an emerging winter crop, this may further restrict the amount of “groceries” put on the crop. I’m skeptical of any massive impact in North America, but it could certainly have an impact in Europe and the MENA region.

This is the second major area of disruption: there is an increasing reality that, with reduced fertilizer use because of high costs or unavailable supplies, global agricultural production could decline in the 2022/23 crop year and even trickle into the 2023/24 crop year. Since this has never really happened in a globalized world that’s dependent on today’s modern farming practices (read: fertilizer usage), this points to some very serious food security situations globally. Put another way, when there is a high cost of food, especially in developing countries that rely on food imports, societal instability usually results, which often leads to regime change (read: more geopolitical unrest!).

The third and final variable I’m considering is the direct impact on the ground in the Black Sea region. Farmers in Ukraine are a few weeks away from planting their spring crop and taking care of emerging fall-seeded crops (if required). Any loans not yet secured for the upcoming growing season are likely up in the air, as is the availability of any fuel, fertilizer, or other crop inputs. Let’s also not forget about the farmworkers/labour who have either fled Ukraine or have risen up and joined the civilian guard there. Thus, there is a major agricultural production risk for Ukraine and this will impact many markets, including wheat, barley, corn, and oilseeds.

From an export standpoint, we know almost every major agricultural player has shut down their facilities in Ukraine and complicating all of this is the aforementioned international payment processing for goods traded. Even if port facilities did re-open, it’ll be very expensive, if not impossible, to get insurance companies to underwrite policies on the cargoes, let alone convince international buyers it’s a safe/secure trade. For the hard winter wheat that Ukraine tends to export, international buyers will likely have to source from either the U.S. or Argentina, both of which have relatively tight exportable supplies today (not to mention, the U.S. HRW wheat belt is in a serious drought). There are also Ukrainian corn and sunflower exports to consider, which again, points to either South or North American substitution, but this is also dependent on competing for similarly-tight supplies. While Russia’s planting campaign will likely be unaffected, their exports will be embargoed in many areas, meaning we’ll see another game of exporter and importer musical chairs.

Given the highly volatile price action, it’s obvious that no one has a clear view on where things are going, as there are so many scenarios that could play out, even including Putin’s removal by his inner circle (AKA a coup). Even if the fighting stopped tomorrow, the ripples of stopped or delayed shipments and payments will certainly be felt for weeks, if not months to come. Therein, it’s certainly likely risk premiums will be added to grain markets, especially in May/June as the Plant 2022 campaign finishes. Thanks to Russia’s action, there’ll be a lot riding on Harvest 2022, even more so than I’ve mentioned in the past. Accordingly, next week, we’ll look at how old and new crop wheat prices are being impacted (as well as any updates to the ongoing situation!).

To growth,

Brennan Turner

Founder | Combyne Ag