July 2025

Wheat Outlook

Upside:

- Canada is showing strong farmer deliveries and record exports into the final weeks of the marketing year.

- North American hard red spring production could be as much as 2 mln tonnes lower in 2025.

- There may be some improvement in global import demand next year, including from Türkiye and China.

Downside:

- Spring wheat conditions are generally improving in both Canada and the US.

- US stocks are projected to be comfortable in 2025/26, including for hard red spring wheat.

- Spring wheat conditions are generally improving in both Canada and the US.Global markets are drifting sideways-to-lower under harvest pressure, while the Canadian seasonal price trend is down.

Key Notes:

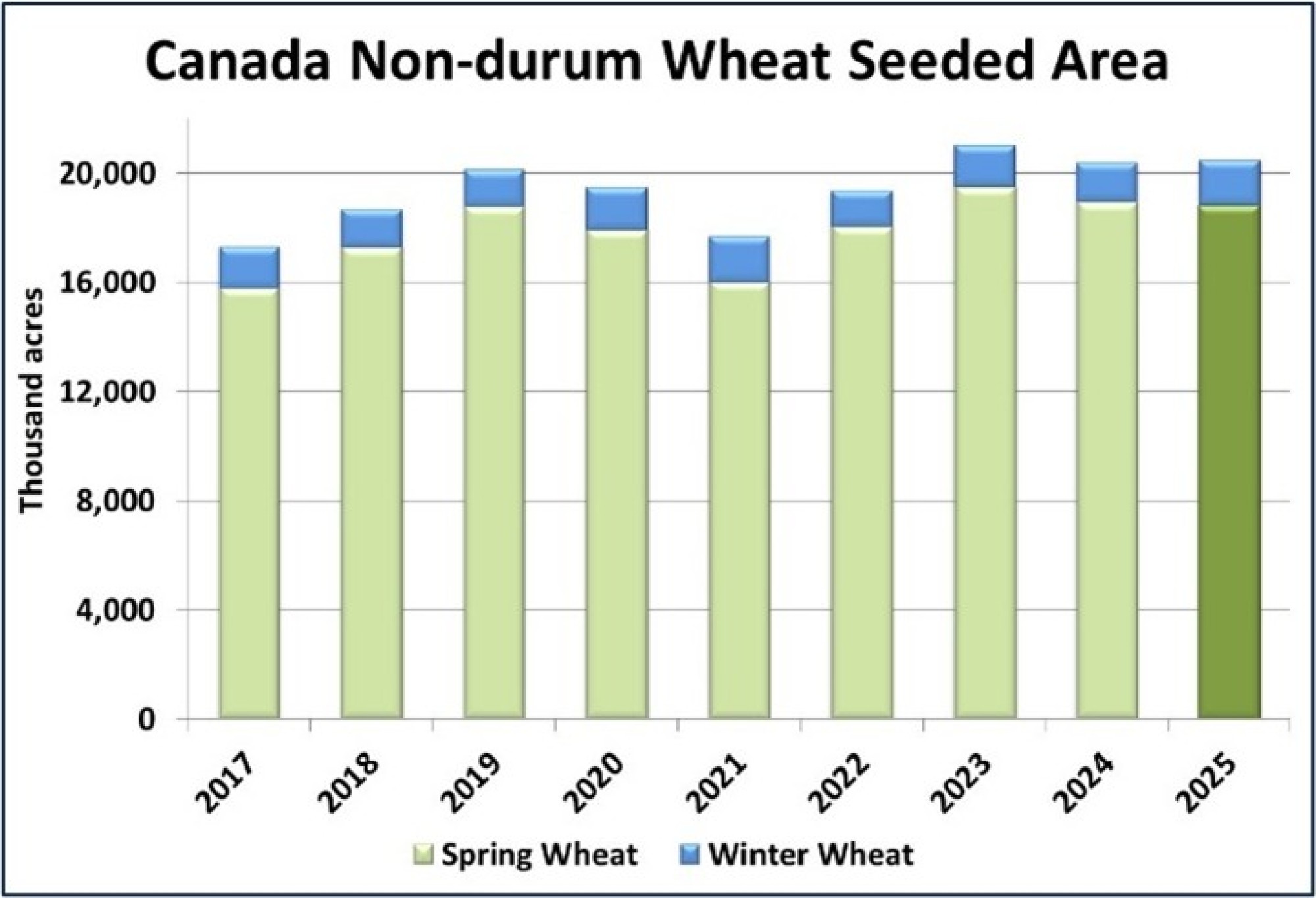

StatsCan reported spring wheat plantings at 18.8 mln acres, below the initial intentions of 19.4 mln. This is the lowest spring wheat area in three years, but well above the 10-year average of 17.5 mln acres. Hard red spring was shown at 15.9 mln acres, 85% of total spring wheat area. While lower acres trims production from initial expectations, of greater importance is crop conditions, with the yield outlook currently improving. Winter wheat acres remaining after winterkill were 1.58 mln, on the upper end of the past 10 years.

- The latest USDA update gave a breakdown for US wheat balances by class. Initial indications point to the 2025/26 carryout increasing for hard red winter and white wheat, while staying essentially flat for hard red spring and soft red winter. Adequate stocks reduce upside price potential in futures markets

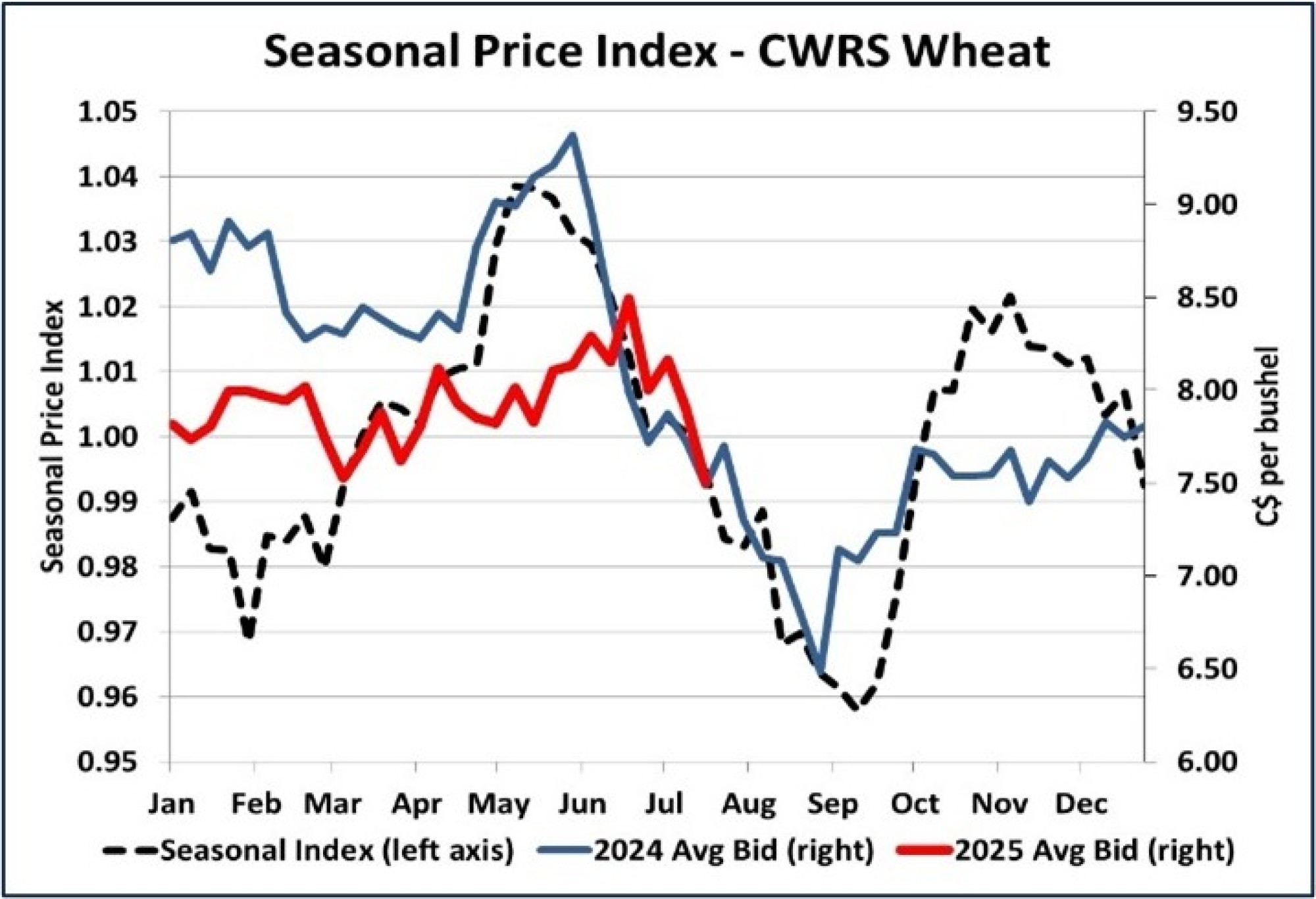

- CWRS prices have turned lower in recent weeks, consistent with the normal seasonal trend. The peak this year came a bit later than normal as dryness in western Canada supported values into mid-June, but the prior strengthening was more muted as well. Barring a significant setback in conditions, values can expect to slide lower into September before carving out a bottom.

Bottom Line:

- The trend remains sideways-to-lower as the Northern Hemisphere winter wheat harvest advances without any major issues and North American spring wheat conditions improve.

- Weakness largely reflects the typical seasonal trend, something exacerbated by a lack of significant production threats.

- Global supplies won’t be burdensome, and eventually prices will carve out a bottom and start to work higher.

Barley Outlook

Upside:

- Canadian barley supplies could be 5% lower in 2025/26, which will likely reduce feed usage.

- Domestic corn prices in China have been trending higher, but barley prices haven't responded yet.

Downside:

- Global barley production is estimated by the IGC at 146.9 mln tonnes, up three mln from last year.

- Sales of Canadian beer have been declining in recent years, reducing maltsters' need for malt barley.

- The recent declines in feed barley bids at Canadian elevators fit the timing of the seasonal index.The US is expected to harvest a record corn crop.

Key Notes:

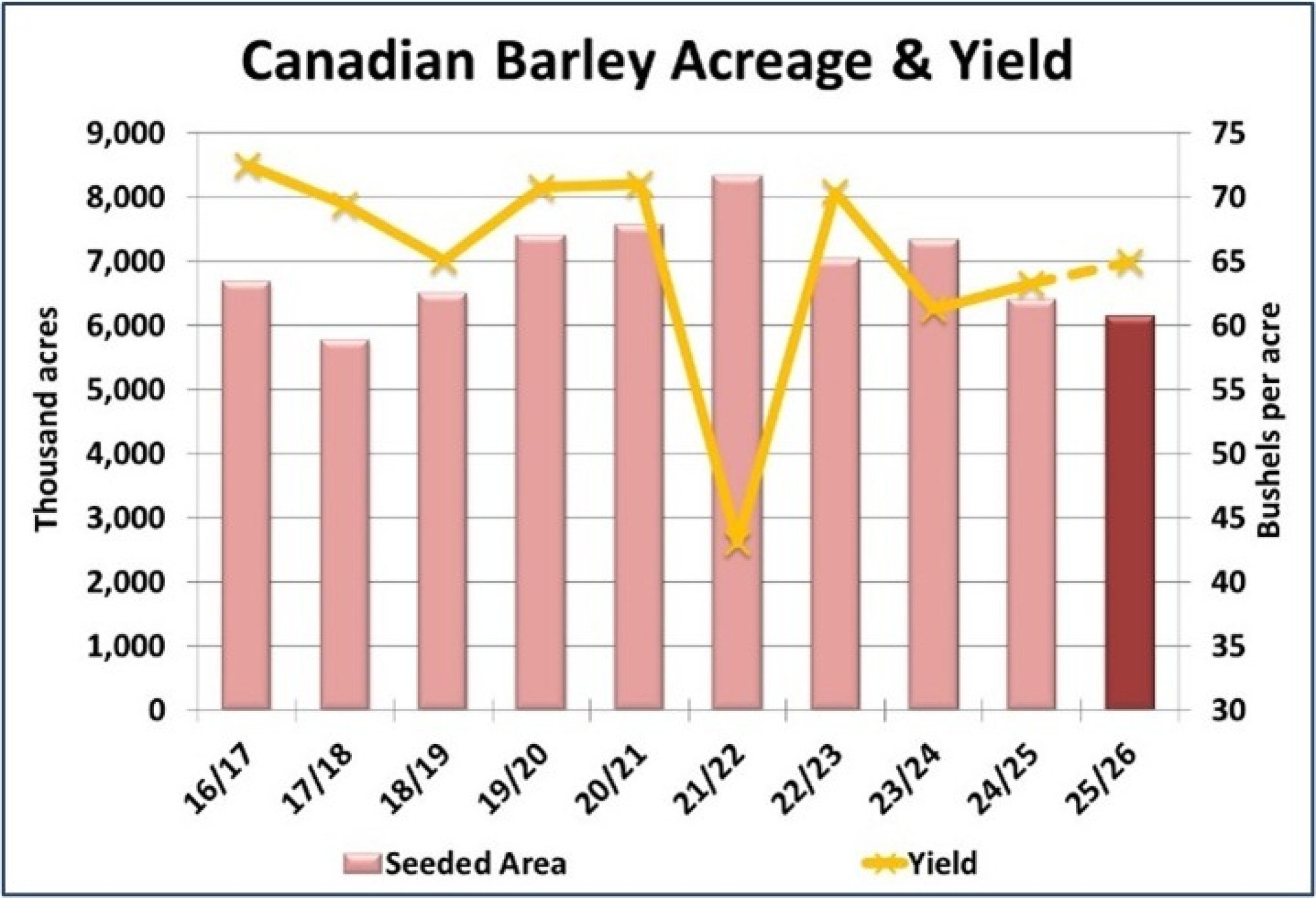

- One surprise in StatsCan’s acreage estimates was the further reduction in barley plantings. StatsCan pegged barley area at 6.1 mln acres, 4% less than last year and the lowest total since 2017/18. Assuming an average yield of 65.0 bu/acre, this puts the 2025 crop at 7.8 mln tonnes, down 4% from last year. This would tighten up supplies and require less domestic feeding, which is quite possible, given cheaper US corn imports. We’ve also trimmed the 2025/26 export forecast to 2.3 mln tonnes, still a bit higher than the current year.

- In its latest monthly report, the IGC trimmed 2025/26 global barley production to 146.9 mln tonnes, but that’s still up from 2024/25 at 143.9 mln tonnes. The largest production declines in the July report were in Türkiye, Russia and Ukraine, while European production was higher by 1.0 mln tonnes. Overall, the global barley situation appears stable, with the IGC forecasting 2025/26 ending stocks at 22 mln tonnes, marginally higher than last year. That said, smaller crops in Russia and Ukraine, two key exporters, could provide a bit more opportunity for Canadian barley shipments.

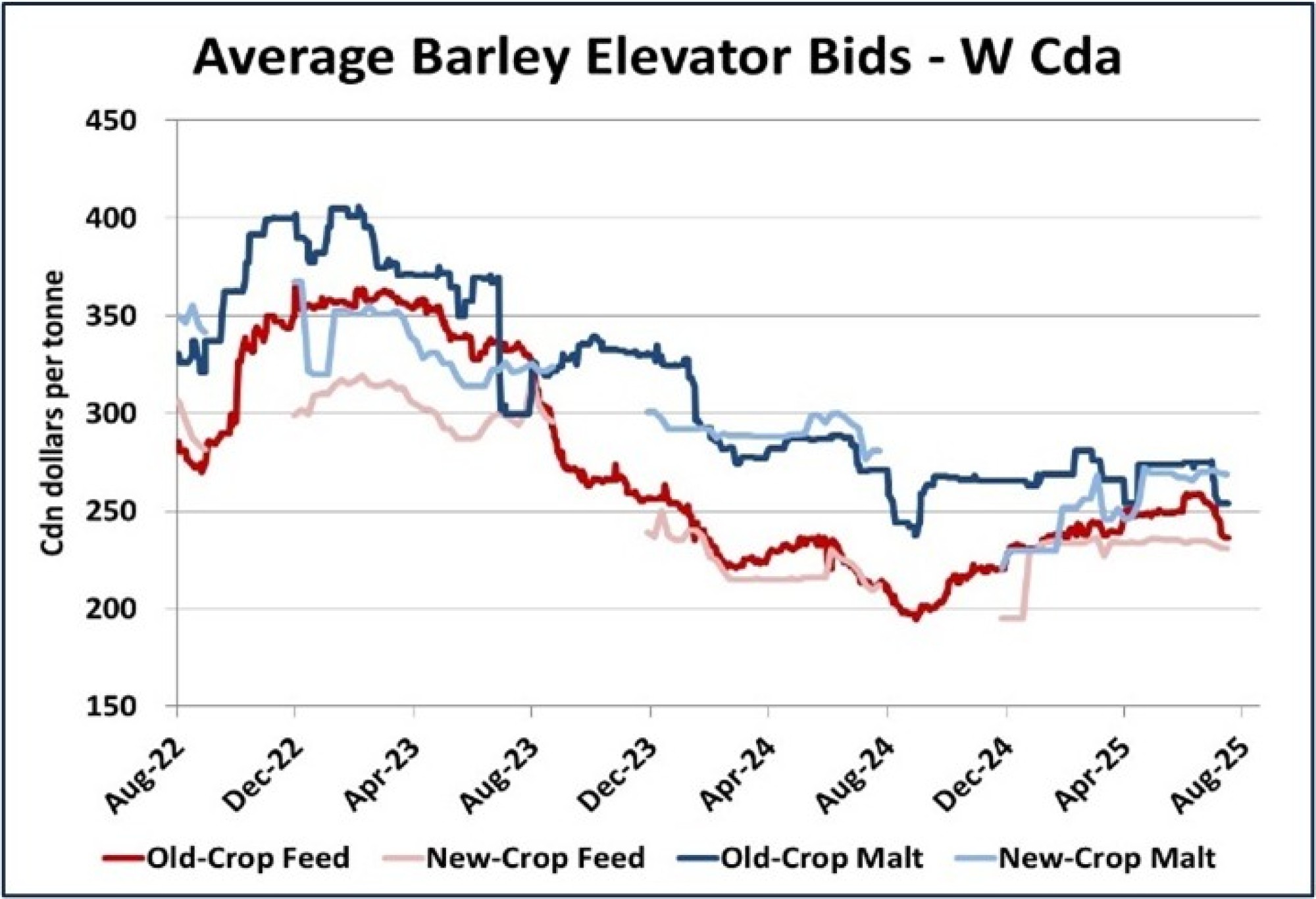

- Average old-crop elevator bids for both feed and malt barley dropped sharply in the last week or two. For feed barley, this move is simply seasonal, as old-crop converges with new-crop price levels. Almost no old-crop malt is trading and the nominal bid has dropped to maintain a typical spread with feed barley. New-crop bids are much steadier for both feed and malt, largely avoiding the drop in corn prices.

Bottom Line:

- Declines in old-crop barley bids are just normal seasonal behavior, with extra pressure coming from the weaker corn market, which could extend the seasonal lows.

- New-crop bids are steady, suggesting buyers are comfortable with the 2025 production outlook, especially if US corn imports can backfill possible shortfalls for domestic feeders.

- The global barley market is still mostly steady, although European prices are coming under pressure due to the ongoing harvest.

- Global barley supplies also appear adequate as long as trade flows are not interrupted. Rising trade tensions with China, the dominant buyer of Canadian barley, have become a key (and sizable) risk factor.

Durum Outlook

Upside:

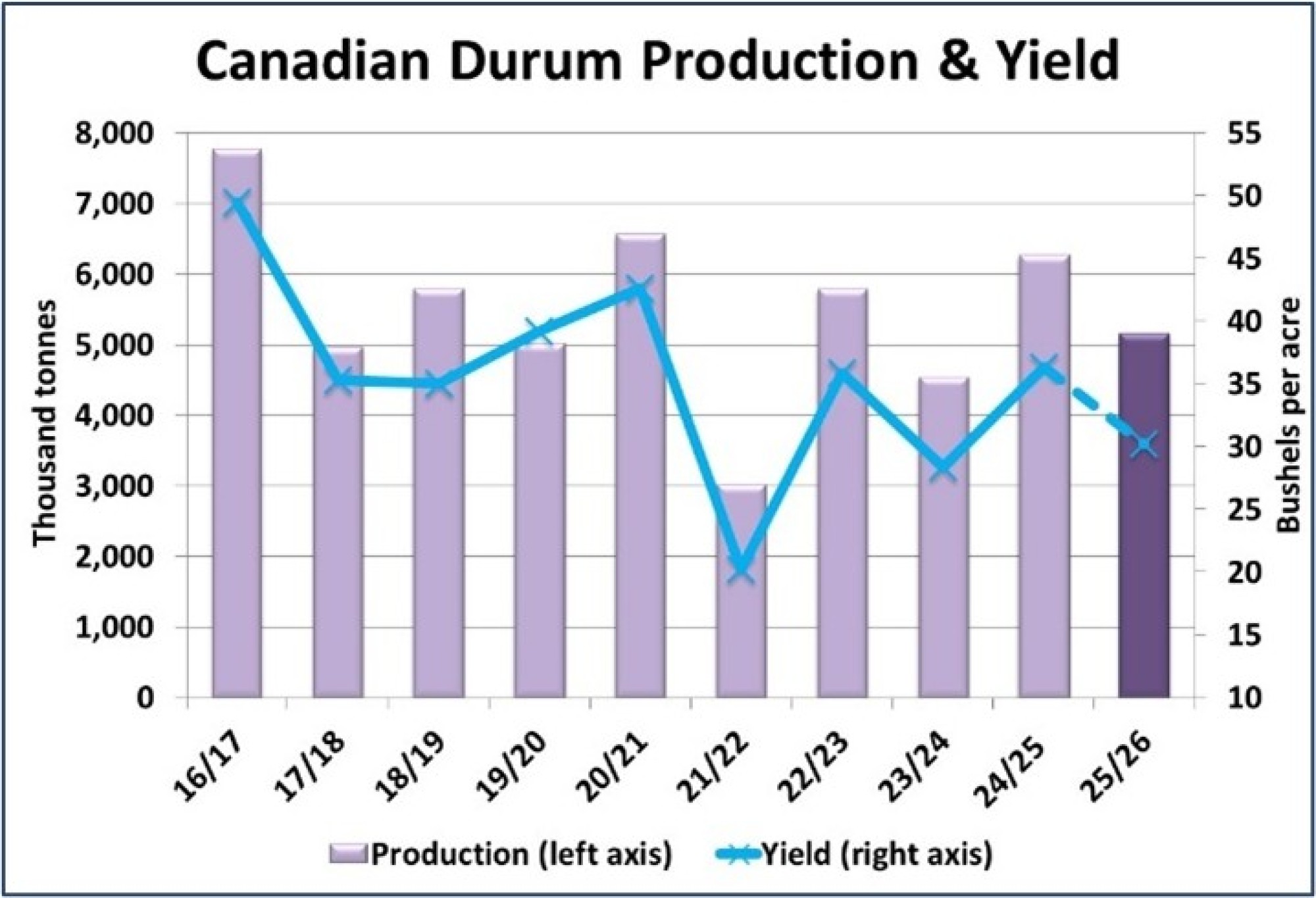

- Canadian durum yield and harvested area estimates are being trimmed, with the 2025 crop now projected at 5.2 mln tonnes

- North Dakota and Montana durum crop ratings are very different, but US production estimates are coming down.

- The US Ag Attaché is estimating a 2025 Turkish durum crop at 3.6 mln tonnes, the lowest since 2021.

Downside:

- The IGC estimated 2025/26 global durum production at 35.9 mln tonnes, unchanged from last year.

- The impact of a smaller Canadian durum crop could be largely offset by reduced demand from key importers, including larger crops in the EU and North Africa.

Key Notes:

- The June rains improved conditions for a number of western Canadian crops, but they missed a good portion of the southern prairies where the durum is grown. As a result, crop ratings for durum remain low. We’ve reduced our yield estimate to 30.2 bu/acre, down from the (adjusted) 2024 yield of 36.3 bu/acre. We’ve also increased abandonment slightly. Our guesstimate of the 2025 crop is now 5.2 mln tonnes, down 1.1 mln (18%) from last year in spite of a 3% increase in seeded area. This caused us to trim the 2025/26 export forecast to 4.6 mln tonnes from 5.7 mln for 2024/25.

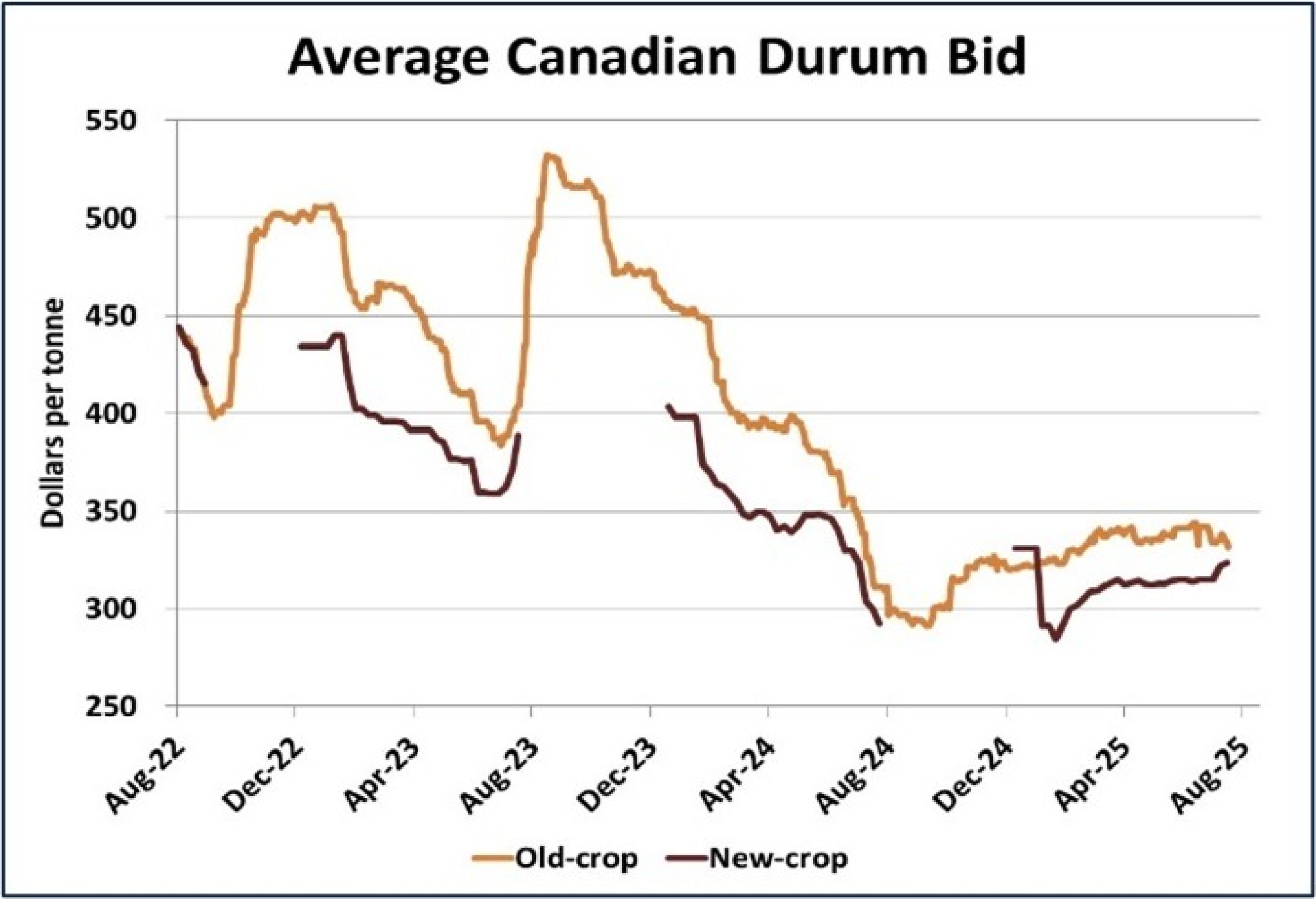

- It’s not all that noticeable on the longer-term chart, but there are some signs that concerns about the 2025 Canadian durum crop are having an impact on durum bids. Old-crop bids are still stuck in a sideways range, as trade gets quieter late in the marketing year and sales are covered, but the average new-crop bid has turned higher.

Bottom Line:

- Steady durum prices are a global phenomenon and that’s keeping Canadian prices from responding more sharply to threats to the North American crop.

- While durum crops in Canada, the US and Türkiye will be smaller in 2025, that’s being offset by increased production in Europe, North Africa and the Black Sea.

- As a result, trade flows will be shuffled but overall supplies seem adequate. Aside from the normal postharvest price recovery, the durum market looks like it’s facing another year of sideways direction.